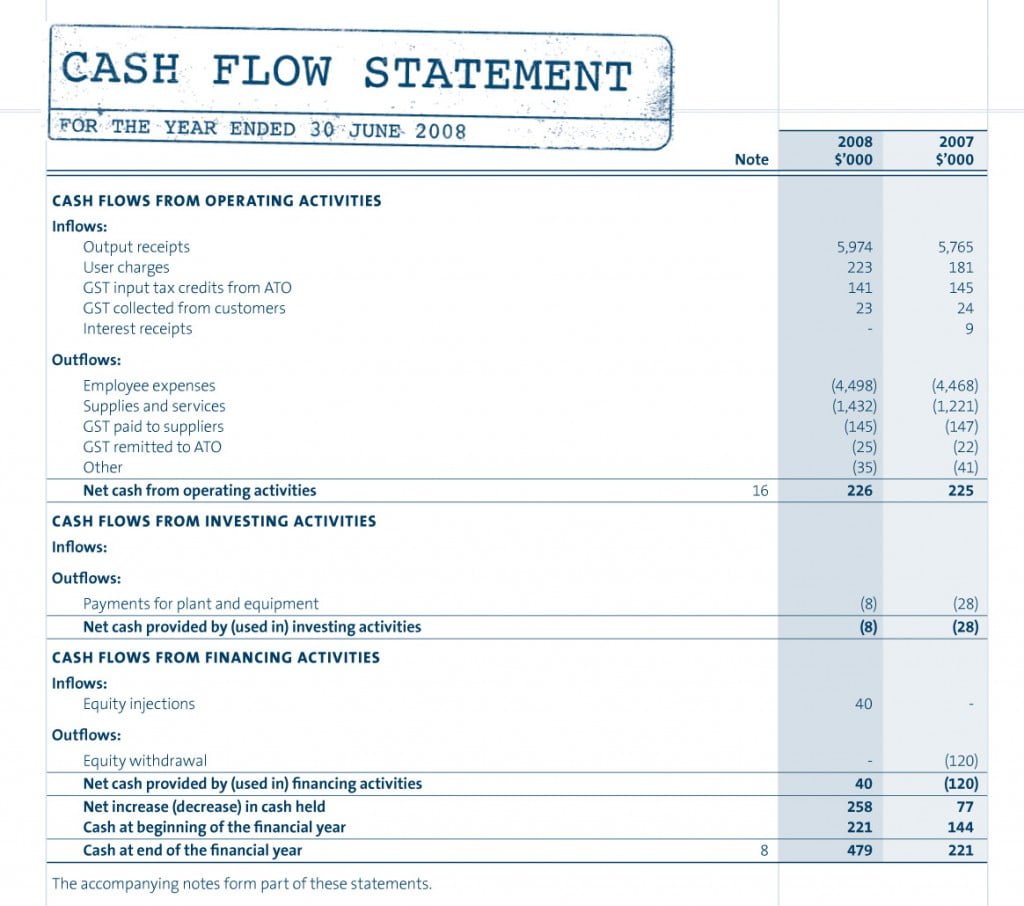

Propensity Company had a noncash investing and financing activity, involving the purchase of land (investing activity) in exchange for a $20,000 note payable (financing activity). As cash is generally viewed by many as the most critical asset to success, this appendix will focus on how to correctly prepare and interpret the statement of cash flows using the direct method. The statement of cash flows is the definitive financial statement to bridge the gaps between revenues and profits, and cash. This method measures only the cash received, typically from customers, and the cash payments made, such as to suppliers. These inflows and outflows are then calculated to arrive at the net cash flow.

- When you have a positive number at the bottom of your statement, you’ve got positive cash flow for the month.

- These inflows and outflows are then calculated to arrive at the net cash flow.

- The items in the operating cash flow section are not all actual cash flows but include non-cash items and other adjustments to reconcile profit with cash flow.

Free Course: Understanding Financial Statements

However, the cash flow statement also has a few limitations, such as its inability to compare similar industries and its lack of focus on profitability. The cash flow statement also encourages management to focus on generating cash. Consequently, the business ended the year with a positive cash flow of $1.5 million and total cash of $9.88 million. This cash flow statement shows that Nike started the year with approximately $8.3 million in cash and equivalents.

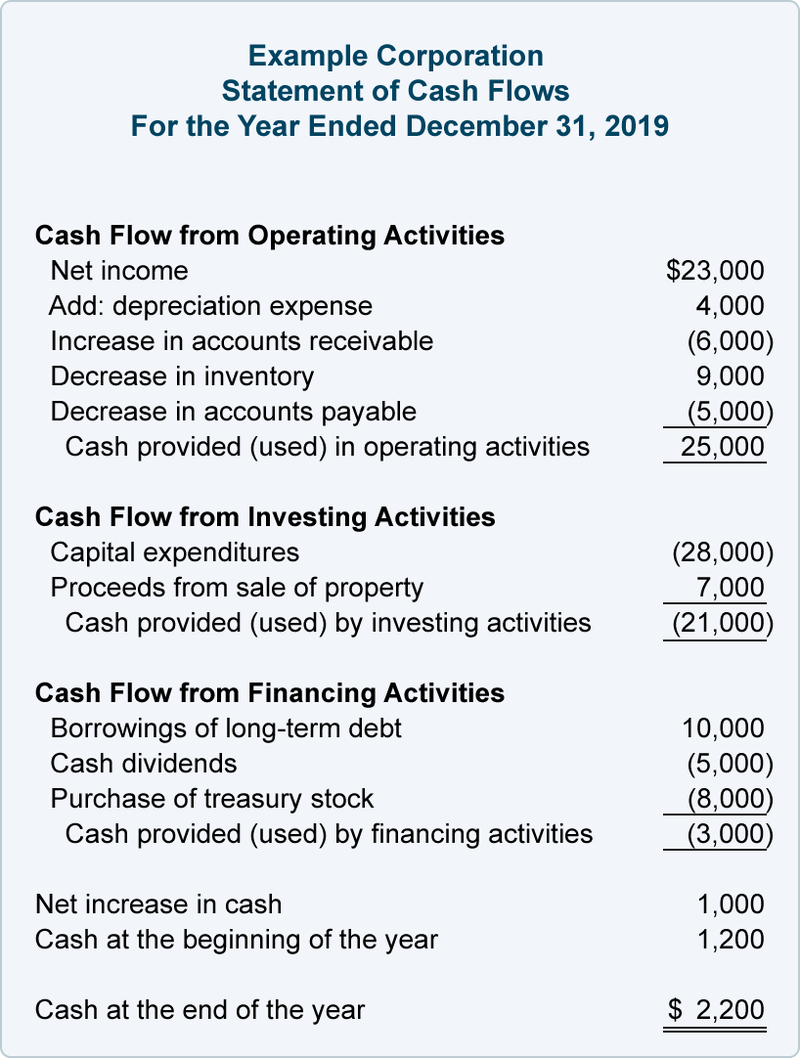

Example of the Statement of Cash Flows Indirect Method

Greg didn’t invest any additional money in the business, take out a new loan, or make cash payments towards any existing debt during this accounting period, so there are no cash flows from financing activities. What makes a cash flow statement different from your balance sheet is that a balance sheet shows the assets and liabilities your business owns (assets) and owes (liabilities). The cash flow statement simply shows the inflows and outflows of cash from your business over a specific period of time, usually a month. Since the income statement and balance sheet are based on accrual accounting, those financials don’t directly measure what happens to cash over a period. Therefore, companies typically provide a cash flow statement for management, analysts and investors to review.

Please Sign in to set this content as a favorite.

The articles and research support materials available on this site are educational and are not intended to be investment or tax advice. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. For information filing a joint tax return when married and living apart pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. Cash flow is the total amount of cash that is flowing in and out of the company.

For that reason, smaller businesses typically prefer the indirect method. The cash flow statement takes that monthly expense and reverses it—so you see how much cash you have on hand in reality, not how much you’ve spent in theory. However, you’ve already paid cash for the asset you’re depreciating; you record it on a monthly basis in order to see how much it costs you to have the asset each month over the course of its useful life. Using only an income statement to track your cash flow can lead to serious problems—and here’s why.

The difference between these methods lies in the presentation of information within the cash flows from operating activities section of the statement. There are no presentation differences between the methods in the other two sections of the statement, which are the cash flows from investing activities and cash flows from financing activities. Increases in current assets indicate a decrease in cash, because either (1) cash was paid to generate another current asset, such as inventory, or (2) revenue was accrued, but not yet collected, such as accounts receivable. In the first scenario, the use of cash to increase the current assets is not reflected in the net income reported on the income statement. In the second scenario, revenue is included in the net income on the income statement, but the cash has not been received by the end of the period. In both cases, current assets increased and net income was reported on the income statement greater than the actual net cash impact from the related operating activities.

For example, in order to figure out the receipts and payments from each source, you have to use a unique formula. The receipts from customers equals net sales for the period plus the beginning accounts receivable less the ending accounts receivable. Similarly the payments made to suppliers is calculated by adding the purchases, ending inventory, and beginning accounts payable then subtracting the beginning inventory and ending accounts payable. Cash flow statements are important as they provide critical information about the cash inflows and outflows of the company. This information is important in making crucial decisions about spending, investments, and credit.

Companies tend to prefer the indirect presentation to the direct method because the information needed to create this report is readily available in any accounting system. In fact, you don’t even need to go into the bookkeeping software to create this report. Let’s take a look at the format and how to prepare an indirect method cash flow statement. The beginning and ending balances that appear on the comparative balance sheet are the same as those in the Equipment ledger’s debit balance column on January 1 and September 12, respectively.

In-depth analysis, examples and insights to give you an advantage in understanding the requirements and implications of financial reporting issues. Textbook content produced by OpenStax is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike License . It might be helpful to look at an example of what the indirect method actually looks like. These materials were downloaded from PwC’s Viewpoint (viewpoint.pwc.com) under license.